“We promised ESOPs eight months ago. The scheme is a Word file, grants are emails, and nobody knows what has vested.”

ESOP management built on Rule 12

ESOPs in India are a legal procedure, not just a promise: a resolution under Sec 62(1)(b), Rule 12 conditions, grant letters, vesting, and perquisite tax at exercise. Saral runs the whole lifecycle and blocks the mistakes that get expensive later.

§ The statute, handled

The Indian-law details, by name.

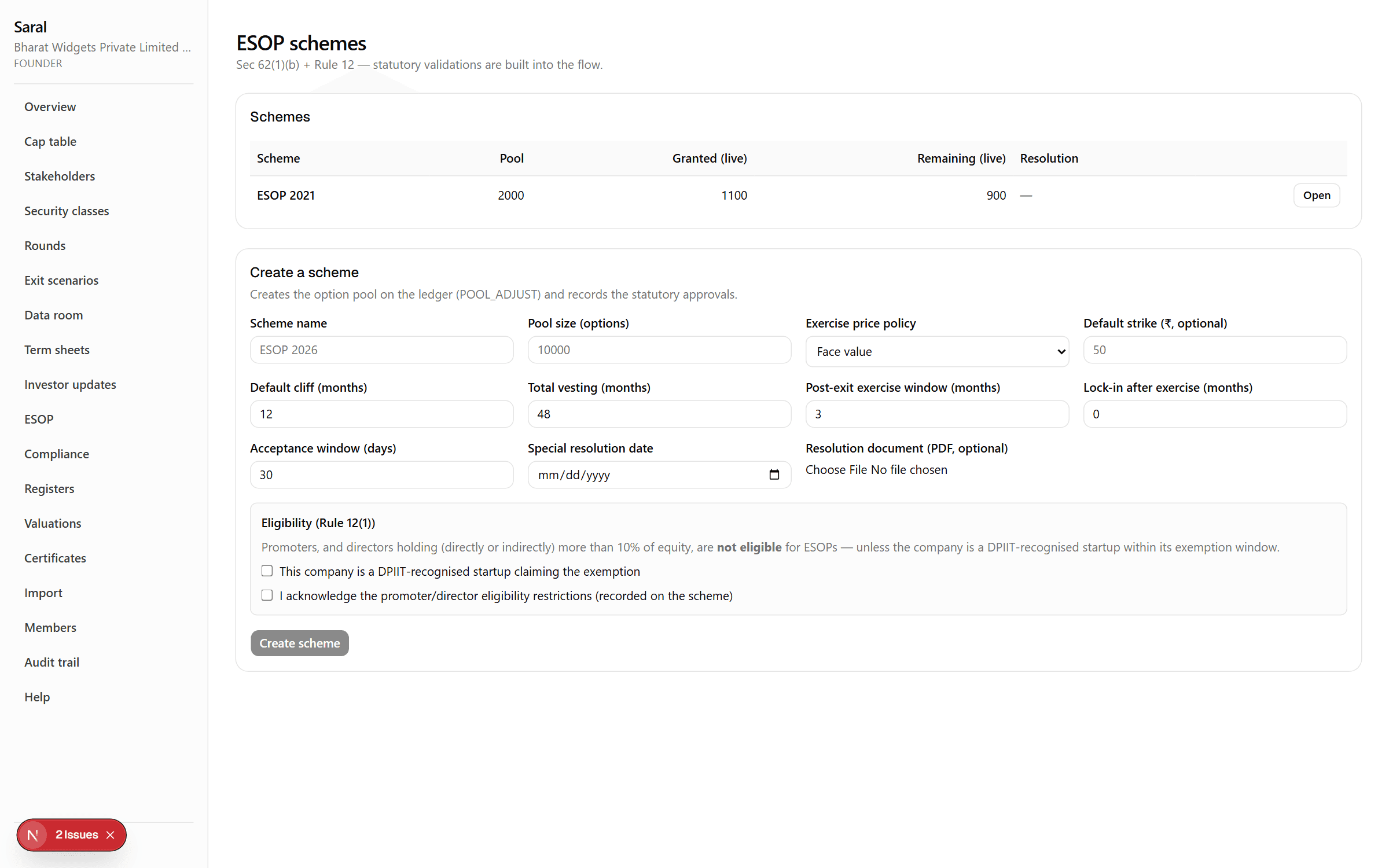

Rule 12 enforced, not suggested

The 12-month minimum cliff is a hard block (no exemptions — confirmed by our reviewing CS). Promoters and directors holding over 10% are blocked from grants unless you record an explicit, logged override.

Perquisite tax, correctly gated

Exercise requires an FMV report from a SEBI-registered Category I merchant banker, dated within 180 days — CA reports do not qualify. Saral blocks exercises that would create TDS exposure.

The 2026 law change, handled

Statements cite the Income-tax Act 1961 or 2025 by event date, and the 80-IAC deferral window is 48 or 60 months depending on when shares were allotted. The deferral only applies with the IMB certificate on file.

Click-wrap acceptance

Grant letters are generated as PDFs; employees accept in the portal with timestamp, IP and document hash recorded.

Questions founders ask

QDoes vesting really run itself?

A daily job computes vesting from each grant’s cliff and schedule, idempotently — re-running never double-counts. You see the same numbers the employee sees.

QWhat about employees who leave?

Termination handling freezes unvested options, applies the exercise window, and the register of options (SH-6) stays correct throughout.

QIs the tax math advice?

No. Saral computes the perquisite and timelines from the statute and shows its working; your CA confirms. Statements say exactly this on their face.

Request a demonstration